The tax return deadline for the 2024 to 2025 tax year is 31 January 2026 for online returns and 31 October 2025 for paper returns. Payment of any tax owed must also reach HMRC by 31 January 2026. Missing these dates can result in automatic penalties and interest charges.

Key takeaways:

- Register for Self Assessment by 5 October 2025 if required

- Submit paper returns by 31 October 2025

- Submit online returns and pay tax by 31 January 2026

- Late filing triggers an immediate £100 penalty

- Further penalties apply after three, six and twelve months

What Is the Tax Return Deadline for 2026 in the UK?

The tax return deadline for 2026 relates to the 2024 to 2025 tax year, which ran from 6 April 2024 to 5 April 2025. HMRC must receive both the tax return and any payment owed by the relevant deadline to avoid penalties.

Key dates include:

- 5 October 2025 to tell HMRC that a return is required if newly liable

- 31 October 2025 for paper tax returns

- 30 December 2025, if requesting to pay through a tax code

- 31 January 2026 for online returns and payment

- 31 July 2026 for second payments on account

Trustees of registered pension schemes and certain non-resident companies must file paper returns by 31 January 2026. Partnerships with a company partner may have different deadlines based on their accounting date.

Filing early after 6 April 2025 helps taxpayers understand what they owe and budget in advance.

Who Needs to Submit a Self-Assessment Tax Return Before the Deadline?

Not everyone in the UK must meet the tax return deadline, as many people pay tax automatically through PAYE. However, individuals and businesses with additional income often need to complete a Self Assessment.

A return is usually required if, during the 2024 to 2025 tax year:

- They were self-employed as a sole trader, earning over £1000

- They were partners in a business partnership

- They had to pay Capital Gains Tax on assets sold

- They were liable for the High Income Child Benefit Charge

- They received untaxed income such as property rent, dividends, savings interest, or foreign income

Some people choose to submit a return voluntarily to claim tax reliefs, pay voluntary National Insurance contributions or confirm self-employment status.

Anyone unsure can check directly with HMRC. If HMRC issues a notice to file, the tax return deadline becomes mandatory.

When and How Should Taxpayers Register for Self Assessment?

Taxpayers who need to file for the first time must inform HMRC by 5 October 2025 following the end of the relevant tax year. This requirement applies if they have not sent a return before or were previously registered but did not need to file for 2023 to 2024.

Registration is completed through the Self Assessment process, after which HMRC issues a Unique Taxpayer Reference. This ten-digit number is essential for accessing the online account and submitting a return. Individuals who previously registered may need to reactivate their accounts to avoid delays.

After registering, taxpayers should begin preparing for their bill. They can estimate the tax due, organise bank statements and receipts, and consider setting aside funds in advance of the 31 January 2026 payment deadline.

How Can the Tax Return Be Submitted Before the Deadline?

Taxpayers can submit their return either online or by post. Most individuals use the online service, which remains open until 31 January 2026.

Submission options include:

- Filing online through the HMRC Self Assessment portal

- Sending a paper return using form SA100

- Using commercial software for partnerships, trusts, non-residents, or complex cases

Paper returns must reach HMRC by 31 October 2025. Online returns can be submitted any time after 6 April 2025 up to the January deadline. If profits are not finalised, provisional figures can be included, but HMRC must be informed and amendments made later if necessary.

Filing early allows taxpayers to see their calculation, arrange payments, and set up a Time to Pay plan if required.

What Are the Penalties for Missing the Tax Return Deadline?

Missing the tax return deadline can result in escalating penalties and interest. HMRC applies separate charges for late filing and late payment, and in some cases for failing to notify liability.

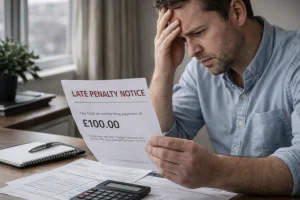

Late Filing Penalties

An automatic £100 penalty is issued if the tax return deadline is missed, even if no tax is owed. This applies immediately after 31 January 2026 for online returns or 31 October 2025 for paper returns.

If the delay continues:

- After three months, daily penalties of £10 per day apply up to a maximum of £900

- After six months, a further penalty of 5 percent of the tax due or £300, whichever is greater

- After twelve months, another 5 percent or £300 charge, whichever is greater

These penalties apply in addition to the original £100 fine. All partners in a partnership may be charged individually if a partnership return is late.

Late Payment Penalties

Paying tax after 31 January 2026 triggers separate charges. HMRC imposes penalties based on how long the amount remains unpaid.

- 5 percent of unpaid tax after 30 days

- An additional 5 percent after six months

- Another 5 percent after twelve months

Interest is also charged from the original due date until the balance is cleared. Even if a return is filed on time, failing to pay by the deadline can become costly. Payments on account due on 31 July are also subject to penalties if unpaid.

Failure to Notify Penalty

If someone should have registered for Self Assessment but failed to notify HMRC by 5 October 2025, they may face a failure to notify penalty. This typically arises where tax remains unpaid after the 31 January deadline.

The penalty is calculated based on the amount of tax still outstanding and is usually issued within twelve months of HMRC receiving the return. The longer the delay and the greater the unpaid amount, the higher the potential penalty.

Penalties must be paid within thirty days of the notice. However, taxpayers who believe they had a reasonable excuse may appeal. Acceptable reasons are considered on a case-by-case basis, but simply overlooking the tax return deadline is unlikely to succeed.

Understanding the structure of penalties highlights why meeting the tax return deadline for 2026 is critical. Filing and paying on time remains the simplest way to avoid additional financial pressure.

How Can Taxpayers Avoid Tax Return Deadline Penalties?

Avoiding penalties starts with early preparation. Taxpayers can submit their return from 6 April 2025, giving ample time before the 31 January 2026 tax return deadline.

Registering by 5 October 2025, where required, prevents failure to notify penalties. Keeping accurate records of income and expenses ensures the return is completed correctly. Estimating the tax bill in advance allows individuals to budget and avoid last-minute stress.

Those concerned about paying in full can explore setting up instalments before the deadline. Filing early also gives time to correct mistakes within the allowed amendment period.

Ultimately, acting promptly and responding to HMRC communications reduces the risk of additional charges and protects financial stability.

What If Someone No Longer Needs to File a Tax Return?

Not everyone who previously completed Self Assessment will continue to need it. However, ignoring the requirement without informing HMRC can still lead to penalties if a notice to file has been issued.

Anyone who believes they no longer need to meet the tax return deadline should notify HMRC as soon as possible.

How to Close Self Assessment Account?

Individuals can sign in to their HMRC online account and complete a form to close their Self Assessment record. They must provide their National Insurance number and Unique Taxpayer Reference. HMRC will review the request and confirm whether future returns are required.

Removing for Specific Year

Taxpayers may ask to be removed from Self Assessment for a particular tax year if circumstances have changed. This request can also be made through the online account. HMRC will assess the details and respond in writing.

Stopping Self-Employment

If someone has stopped trading as a sole trader, they must inform HMRC separately that their self employment has ended. Even after notifying HMRC, a final return may still be required. Failure to communicate these changes before the tax return deadline could result in automatic penalties.

No Longer Renting Property

Landlords who have stopped renting out property should inform HMRC if rental income was the only reason for filing. Untaxed income such as rent often triggers Self Assessment. Once it ceases, removal may be possible, but confirmation from HMRC is essential.

Child Benefit Charge Changes

Some individuals previously filed solely because of the High Income Child Benefit Charge. Where arrangements change, and the charge is handled differently, they may no longer need to submit a return. HMRC must still be informed formally to prevent future notices being issued.

Importance of Notifying Before 31 January

Timing is crucial. HMRC needs time to review requests before the 31 January 2026 tax return deadline. If a notice to file remains active and no return is submitted, automatic late filing penalties can apply.

Taxpayers can track the progress of their request within their online account. HMRC will confirm in writing whether a return is still required. Acting early protects against unnecessary fines and ensures compliance with official guidance.

Can a Tax Return Be Changed After Submission?

Yes, taxpayers can amend a return within twelve months of the Self Assessment deadline. For the 2024 to 2025 tax year, changes are generally allowed until 31 January 2027.

Key points include:

- Online returns can be updated after waiting seventy-two hours

- Corrections can be made through the Self Assessment account

- Paper returns require amended pages marked clearly

- If tax increases, interest may apply from the original due date

- Overpayments may result in a refund

If more than twelve months have passed, individuals must write to HMRC to report underpaid income or claim overpayment relief. Claims for overpayment relief can be made up to four years after the end of the relevant tax year.

What Happens If the Taxpayer Has Died?

When a taxpayer dies, the personal representative becomes responsible for dealing with their tax affairs. HMRC may require a Self Assessment return for income earned before death and possibly another for income generated by the estate.

The representative should use the Tell Us Once service to notify government departments. HMRC will confirm whether a return is needed and provide instructions. Information required may include bank statements, pension details and employment records.

The completed return must be sent by post and received by the date stated in HMRC correspondence.

If the estate earns further income, it may need to be registered separately. Professional assistance can be used, but the legal responsibility rests with the personal representative.

How Does Making Tax Digital Affect Future Tax Return Deadlines?

Making Tax Digital for Income Tax will gradually replace the traditional Self Assessment process for certain taxpayers. The rollout begins in April 2026 for those earning over £50000 from self-employment or property income.

Thresholds will reduce to £30000 from April 2027 and £20000 from April 2028. Affected individuals will need to keep digital records and submit updates to HMRC more frequently using approved software.

HMRC will use information from the 2024 to 2025 return to determine who must comply. Those below the thresholds may continue with Self Assessment for now. Preparing early ensures businesses can adapt before new reporting obligations take effect.

Final Thoughts on the Tax Return Deadline 2026

The tax return deadline for 2026 is clear. Paper returns must reach HMRC by 31 October 2025, and online returns and payments must be completed by 31 January 2026. Registration by 5 October 2025 is essential for new filers.

Penalties for missing the tax return deadline escalate quickly, beginning with an automatic £100 fine. Additional charges and interest can follow if delays continue.

Filing early, budgeting carefully, and communicating with HMRC if circumstances change are the most reliable ways to stay compliant. Acting now reduces stress and protects against avoidable costs.

FAQs

What time is the tax return deadline on 31 January 2026?

The online tax return deadline is 11.59 pm on 31 January 2026. Payments must also reach HMRC by that time to avoid penalties.

Can the tax return deadline be extended?

HMRC does not routinely extend the tax return deadline. Extensions are only considered in limited circumstances and usually require a valid reason.

What is a Unique Taxpayer Reference?

A Unique Taxpayer Reference is a ten-digit number issued by HMRC when registering for Self Assessment. It is required to access and submit a tax return.

How long should tax records be kept?

Self-employed individuals must keep records for at least five years after the tax return deadline. Others generally need to keep records for at least twenty-two months after the end of the tax year.

Can penalties be cancelled?

Penalties may be appealed if there is a reasonable excuse. HMRC reviews each case individually before deciding whether to cancel a charge.

What is a payment on account?

A payment on account is an advance payment towards the next tax bill. It is usually due in two instalments on 31 January and 31 July.

How long does a tax refund take?

Refund times vary depending on circumstances and checks required. The status can be viewed in the online tax account.