Picture a self-employed graphic designer in Leeds, settling down after a long invoicing session, who decides to unwind for half an hour on a slots site. Before the first spin loads, a prompt asks whether he wants to set deposit limits.

It is a small moment, easily clicked past, yet it sits at the heart of a sprawling system of UK consumer protections that touches everything from credit agreements to DWP benefit safeguards. Most people never think about the machinery behind that prompt until they bump up against it.

That machinery includes Gamstop, the national scheme that lets people block themselves from licensed British gaming websites for a fixed period.

Once someone signs up, domestically licensed operators are required to turn them away. This is precisely why a growing number of UK readers ask about the non gamstop casino category offshore-licensed sites, often regulated in places like Curaçao, that operate outside the British blocking scheme entirely.

Reviews of the newer 2026 entrants tend to focus on bigger welcome bonuses, broader game libraries, crypto deposit options and quicker withdrawals than their domestically regulated counterparts.

Understanding what these sites are, and how they differ from UK-licensed ones, matters to anyone trying to make sense of where consumer protections start and stop.

A Web of Rules, Not a Single Rulebook

UK consumer protection is rarely one tidy document. It is a patchwork stitched together by overlapping bodies, each with its own remit.

The Financial Conduct Authority watches over lending and credit. Trading Standards handles unfair commercial practices. The Money and Pensions Service runs free guidance for people drowning in debt. Gaming oversight sits alongside all of this, not above it.

For the average household, these systems only become visible at moments of friction a declined credit application, a refunded faulty appliance, a letter from a debt charity.

The gaming side works much the same way. Tools like deposit caps, reality-check reminders and the Gamstop block are designed to be invisible until needed.

They form one corner of a far larger consumer-safeguarding effort, the same effort that produces energy price caps and rules on misleading supermarket pricing that this publication’s readers follow closely.

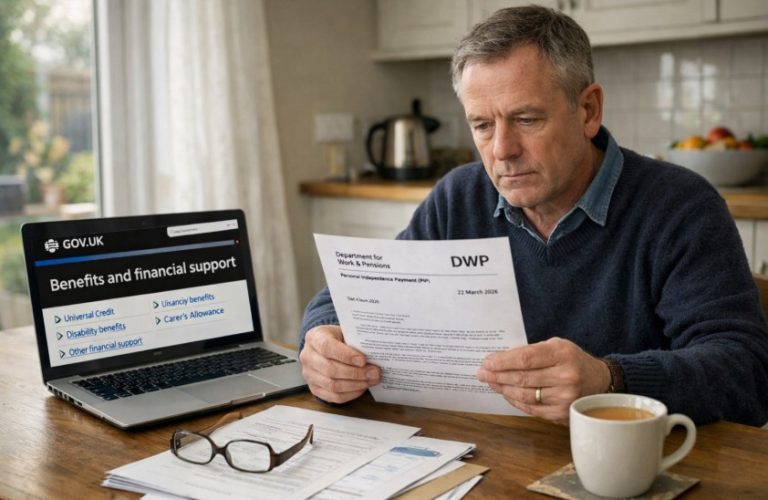

Where the DWP Quietly Enters the Story?

The Department for Work and Pensions does not regulate gaming, yet its fingerprints appear on the edges of the conversation. DWP staff handling Universal Credit and PIP claims are increasingly trained to spot signs of financial harm, and budgeting support for vulnerable claimants now routinely references compulsive spending.

When a claimant’s outgoings raise concern, the safeguarding response draws on the same consumer-protection logic that underpins gaming controls.

There is also the practical question of money flow. Benefit payments land in the same current account that funds everyday spending, which is why banks now offer their own gambling-block features that customers can toggle on.

A claimant managing a tight monthly budget might switch on a bank block, set a card freeze, or use a budgeting app each a small lever in a wider system meant to keep spending in check.

The DWP’s role is less about policing and more about signposting, pointing people toward help before a problem hardens. It is the kind of early intervention that echoes research into keeping customers loyal, where acting before someone walks away tends to cost far less than winning them back.

Why Some Players Look Beyond the British System?

The offshore question is where business and finance readers tend to lean in. Sites licensed abroad are not bound by Britain’s blocking scheme, which is exactly the point of difference reviewers highlight.

They can offer larger sign-up promotions, accept Bitcoin and stablecoins, and process withdrawals on a different timetable, because they answer to a different regulator in a different jurisdiction.

For businesses, there is a useful parallel here in how loyalty is built and held. Offshore operators compete fiercely on generosity precisely because they cannot rely on a captive domestic market.

That mirrors the broader commercial lesson in building loyalty online, where standing out means giving people a reason to stay rather than assuming they have nowhere else to go. The same competitive pressure that produces flashier bonuses also produces churn and churn is the enemy of any subscription or membership model.

The Business Lesson Hiding in the Detail

Strip away the gaming context and what remains is a study in trust, friction and choice themes any small business owner recognises.

A customer who feels protected tends to stay; one who feels trapped tends to leave the moment a better offer appears. Time and again, the same point surfaces: retention is cheaper than acquisition, and goodwill compounds over time.

The contrast between heavily regulated domestic sites and lighter-touch offshore ones is, in commercial terms, a contrast between two retention philosophies.

One leans on compliance and consumer reassurance; the other leans on generosity and speed. Neither is a guaranteed winner, which is why understanding how retention helps small businesses grow is worth more than any single bonus headline. The principle travels across industries from energy tariffs to email marketing lists.

Reading the Landscape With Clear Eyes

For the Leeds designer clicking past that deposit prompt, none of this is front of mind. Yet the prompt, the bank block, the DWP signposting and the offshore alternatives all belong to the same story: a country trying to balance personal freedom against personal protection, with consumers left to navigate the gaps between them.

The clearer that picture becomes, the better-equipped readers are to make informed choices whether they are managing a household budget, running a small firm, or simply weighing up where the safeguards in their own financial life begin and end.