Making Tax Digital will not reduce your State Pension or private pension directly. However, if you are retired and earn extra money from rental property or self-employment, you may soon need to keep digital records and send quarterly updates to HM Revenue and Customs.

From April 2026, landlords and sole traders with more than £50,000 of qualifying income will need to join the new system. The threshold then falls to £30,000 in 2027 and £20,000 in 2028.

Key points:

- Pension income alone is not included

- Rental income and self-employment income are included

- Many retired landlords could be affected

- You may need software or an accountant

- Some people can apply for an exemption if they are digitally excluded

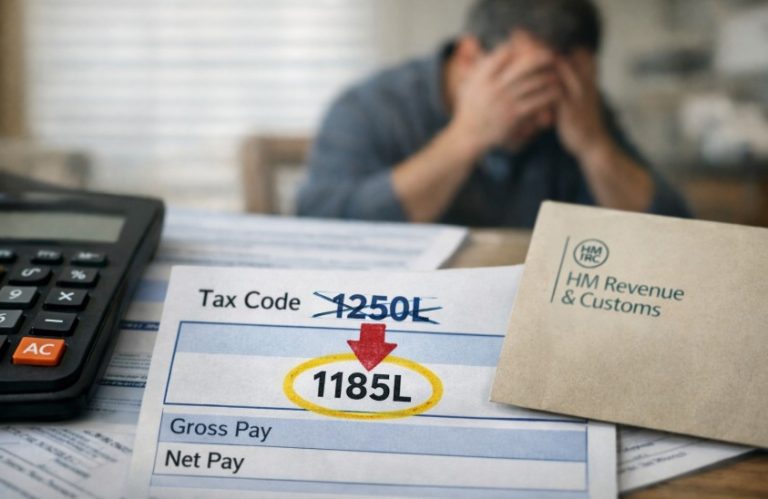

What Is Making Tax Digital and Why Does It Matter to Your Pension?

Making Tax Digital for Income Tax is a new way of reporting self-employment and property income to HM Revenue and Customs. Instead of keeping paper records and sending one Self Assessment return each year, you will need to keep digital records and send updates every quarter using approved software.

This matters to your pension because many people in retirement rely on rental income, freelance work or part-time self-employment to supplement their pension. While your State Pension and private pension are not directly changing, any extra income from a buy-to-let property or side business could bring you into the new system.

If you receive only pension income, you do not need to use Making Tax Digital. The rules apply only if you are a sole trader, landlord or both, and your qualifying income is above the required threshold.

How Could Making Tax Digital Affect Pensioners With Rental Income?

If you are retired and own a rental property, Making Tax Digital could change the way you manage your finances. You may have to move from paper files and annual tax returns to digital bookkeeping and quarterly submissions.

For many pensioners, the concern is not higher tax. The concern is the extra time, cost and administration involved.

You may need to:

- Keep digital records of every rent payment and expense

- Submit updates to HMRC four times a year

- Learn how to use accounting software

- Pay for an accountant or bookkeeping service

Some pensioners may find this manageable. Others may feel it creates too much pressure, especially if they are less confident using computers.

One retired landlord described the changes by saying:

“Quarterly reporting, software costs, accountant fees and the fear of getting it wrong all add up. For many smaller landlords, especially those less comfortable with technology, it feels like a step too far. And crucially, it is landing at the worst possible moment.”

That reflects the main concern for many older landlords: the rules may not reduce pension income directly, but they could make keeping a rental property less worthwhile.

Who Will Need to Use Making Tax Digital for Income Tax From 2026?

From 6 April 2026, Making Tax Digital becomes mandatory in phases. The date you need to join depends on how much property or self-employment income you receive.

To be affected, all of the following must apply:

- You are registered for Self Assessment

- You receive income from property, self-employment or both

- Your qualifying income is above the relevant threshold

Your pension income is not included in this figure. Only property and self-employment income count.

Will You Need to Join if Your Property or Self-Employment Income Exceeds £50,000?

If your qualifying income was more than £50,000 in the 2024 to 2025 tax year, you will need to use Making Tax Digital from 6 April 2026.

For example, you may need to join if you:

- Receive more than £50,000 in rent from one or more properties

- Earn over £50,000 from self-employment

- Have combined property and self-employment income above £50,000

You will still need to file your normal Self Assessment return for the 2025 to 2026 tax year. The new digital system begins after that. HMRC will usually write to you if your income is above the threshold, but you remain responsible for checking yourself.

What Happens if Your Income Is Between £30,000 and £50,000?

If your income is between £30,000 and £50,000, you will not usually need to join in 2026. Instead, you are likely to be brought into the system from 6 April 2027.

This applies if your qualifying income in the 2025 to 2026 tax year is more than £30,000.

You may still have time to prepare by:

- Reviewing your rental income now

- Choosing software early

- Speaking to an accountant before the rules begin

Many retired landlords fall into this category because they own one or two properties that provide modest additional income alongside a pension. According to recent reporting, many people are already considering whether the extra administration is worth it.

One comment often repeated by small landlords is:

“For some, the sums no longer work. For others, the hassle no longer feels worth it. The result is not a dramatic sell-off that grabs headlines, but a slow retreat.”

This reflects growing concern that some smaller landlords could leave the market before the lower threshold begins.

How Will the £20,000 Threshold in 2028 Affect More Pensioners?

The biggest change arrives in April 2028, when the threshold is expected to fall again to £20,000.

That means many more pensioners and part-time landlords could be included, especially if they:

- Own a single rental property

- Rent out a former family home

- Earn occasional self-employment income after retirement

Someone with rental income of £22,000 a year from one flat may not be affected in 2026 or 2027, but could need to join in 2028. This lower threshold is expected to affect nearly 3 million people across the UK.

| Tax Year Reviewed | Qualifying Income Threshold | Start Date for Making Tax Digital |

|---|---|---|

| 2024 to 2025 | Over £50,000 | 6 April 2026 |

| 2025 to 2026 | Over £30,000 | 6 April 2027 |

| 2026 to 2027 | Over £20,000 | 6 April 2028 |

Why Are Small Landlords and Retirees Worried About the New HMRC Rules?

Small landlords are worried because the new rules arrive at a time when running a rental property is already more expensive.

Mortgage rates, insurance costs, maintenance bills and tax changes have all increased in recent years. Making Tax Digital adds another layer of administration.

Many pensioners own just one property and use the rent to top up a modest retirement income. They often do not think of themselves as business owners, yet they may still need to comply with the same reporting rules as larger landlords.

Another concern is that bigger landlords already use digital systems and accountants, so the changes may affect them less.

One property owner summed up the concern this way:

“What pushes a small landlord out barely registers for a bigger one. The balance shifts. And tenants feel it.”

That is why critics believe the rules may have a greater impact on retired landlords than on large property companies.

What Extra Costs Could Making Tax Digital Create for Pensioners?

Making Tax Digital is designed to modernise the tax system, but it could also create new costs for retired landlords and self-employed pensioners.

These costs may not be huge on their own, but together they could reduce the value of the extra income you rely on in retirement.

Will You Need To Pay for Accounting Software or an Accountant?

Most people affected by Making Tax Digital will need software that can connect to HMRC. There are free and paid options, but many pensioners may choose paid software because it is easier to use.

Typical costs may include:

- Free software with limited features

- Paid software costing around £5 to £8 per month

- Accountant fees for quarterly submissions

- Extra charges if you need help setting up the system

HMRC says you can still use spreadsheets if you connect them to approved bridging software. However, many people may prefer to pay an accountant instead.

For a pensioner with one rental property, even an extra £100 to £300 a year in software and accountancy costs may feel significant.

Could Quarterly Reporting Increase Stress and Administration?

The biggest change is that you will no longer simply keep records until January each year. Instead, you will need to send four quarterly updates and then complete a final declaration.

This could mean:

- More deadlines to remember

- More paperwork throughout the year

- A greater risk of making mistakes

- Additional pressure if you are not confident with technology

The first quarterly deadline for people joining in April 2026 is expected to be 7 August 2026. After that, updates will normally be due every three months.

The likely deadlines are:

- 7 August

- 7 November

- 7 February

- 7 May

Although HMRC has said the first year will be more flexible, there will eventually be penalty points for missing deadlines. A £200 fine applies once you reach four points.

Might Some Pensioners Decide To Sell Their Rental Property?

For some people, the new rules may become the final reason to leave the rental market.

This does not mean everyone will sell. However, some pensioners may decide that:

- The extra administration is not worth the effort

- Their property no longer provides enough profit

- They would rather simplify their finances in retirement

If more older landlords sell, the supply of rental homes could fall. That may increase rents and reduce choice for tenants.

Some reports suggest this process may happen slowly rather than suddenly. One landlord may sell a property. Another may stop renting it out. A third may deliberately keep their income below the threshold.

Over time, that could change the shape of the rental market and reduce the number of smaller, independent landlords.

How Will Making Tax Digital Change the UK Rental Market?

Making Tax Digital could gradually reduce the number of small landlords in the private rental sector. Many older landlords already face higher costs and tighter rules. If some decide to sell or stop renting, fewer homes may be available.

This may lead to:

- Higher rents in some areas

- Less choice for tenants

- More large landlords and companies in the market

- Fewer small, family-run rental businesses

Larger landlords are less likely to be affected because they already use accounting software and professional advisers. By contrast, many pensioners still keep paper records or complete one annual tax return. The shift to quarterly digital reporting may therefore affect them more strongly.

The wider concern is that a tax change designed to improve efficiency could also change who remains in the rental market over the next few years.

Who Is Exempt From Making Tax Digital for Income Tax?

You may not need to use Making Tax Digital if you are exempt. An exemption means you can continue using the normal Self Assessment process instead.

You could be exempt if it is not reasonable for you to use digital tools because of:

- Your age

- A disability or health condition

- Poor internet access

- Religious beliefs that prevent digital communication

You are also exempt if you only receive pension income and no property or self-employment income. Even if you are exempt, you still need to complete a Self Assessment return if required. The exemption only removes the digital reporting requirement.

Some groups also have temporary exemptions, including certain carers and people receiving specific tax reliefs.

Importantly, simply saying that you are older is unlikely to be enough. HMRC will normally want evidence that your age or circumstances genuinely make digital reporting unreasonable.

What Should You Do if You Are Digitally Excluded or Struggle With Technology?

If you are worried about using computers, you are not alone. Many pensioners who rely on rental income have never used bookkeeping software before. The good news is that there are still options available.

Can You Apply for an HMRC Exemption?

You may be able to apply for an exemption if it is not reasonably practical for you to use digital software.

HMRC may consider an exemption if:

- You have limited internet access

- You have a disability or health condition

- Your age makes it difficult to use digital tools

- You live in a remote area without reliable broadband

You must apply directly to HMRC rather than simply assuming you are exempt. Until your exemption is approved, you should continue preparing for Making Tax Digital.

What Evidence Might HMRC Ask You To Provide?

HMRC may ask you to explain why you cannot reasonably use digital systems.

You may need to provide:

- Medical evidence if a health condition affects you

- Information about poor broadband or no internet access

- Details showing why your age affects your ability to comply

- Confirmation of any religious reason

The decision is made case by case.

For example, a retired landlord in their late seventies who has no internet connection and struggles to use a smartphone may have a stronger case than someone who simply prefers paper records.

What Are Your Options if a Family Member or Tax Agent Helps You?

You do not always need to manage the system on your own.

You could ask:

- A family member to help with the software

- A trusted friend to keep records

- An accountant or tax adviser to file updates for you

HMRC also allows tax agents to act on your behalf. If you already use an accountant for Self Assessment, they may be able to manage the new quarterly updates too. This can reduce stress and make it easier to stay compliant, although it may increase your annual costs.

How Can You Prepare for Making Tax Digital Before the Deadline?

The best approach is to prepare early rather than waiting for HMRC to contact you.

You should:

- Check your property and self-employment income

- Work out whether you are likely to cross the threshold

- Decide whether you need software or an accountant

- Start keeping simple digital records now

HMRC says it will usually send a letter if your income is above the threshold. However, you remain responsible for checking whether the rules apply to you.

If you think you may be affected, now is a good time to gather your paperwork, speak to your accountant and consider whether you may qualify for an exemption.

Real-Life Example: How Making Tax Digital Could Affect a Retired Landlord

Imagine you are 68 and receive:

- A State Pension

- A small private pension

- £36,000 a year in rent from a former family home

Your pension income does not count towards Making Tax Digital. However, your rental income does. Because your property income is above £30,000, you would probably need to join the system from April 2027.

That means you may need to:

- Buy approved software

- Learn how to keep digital records

- Send four updates to HMRC each year

- Possibly pay an accountant for support

If you already find online banking difficult, this could feel overwhelming. However, you may still have choices. You could apply for an exemption if you are digitally excluded.

You could ask a family member to help. Or you could use an accountant and continue keeping your property as part of your retirement plan.

The key point is that Making Tax Digital does not automatically threaten your pension. The real issue is whether the extra reporting requirements make it harder or more expensive to manage your additional income.

Conclusion

Making Tax Digital is unlikely to reduce your pension directly, but it may affect the way you manage rental income or self-employment income in retirement.

If you rely on extra income from property, now is the time to understand the rules. Check whether your income is likely to exceed the thresholds, explore software options and speak to an accountant if needed.

You should also consider whether you may qualify for an exemption if technology is difficult for you.

The earlier you prepare, the easier the transition is likely to be. By taking action before the deadlines arrive, you can protect your pension income, avoid unnecessary stress and decide whether keeping your rental property still works for your retirement plans.

FAQs

Could Making Tax Digital reduce my State Pension payments?

No, Making Tax Digital does not reduce your State Pension or private pension. It only changes how you report rental or self-employment income to HMRC.

Do I need to use Making Tax Digital if I only receive pension income?

No, you do not need to use Making Tax Digital if your only income comes from a State Pension or private pension. The rules apply only to people with qualifying property or self-employment income above the threshold.

What happens if I miss an HMRC quarterly update?

If you miss a quarterly update, HMRC may give you a penalty point under its new system. Once you collect enough points, you could receive a financial penalty.

Can I still complete a normal Self Assessment tax return?

Yes, you will still need to complete a final declaration or Self Assessment-style submission at the end of the tax year. Making Tax Digital adds quarterly updates rather than removing year-end reporting completely.

Will Making Tax Digital apply to jointly owned rental properties?

Yes, jointly owned rental properties can still count towards the threshold if your share of the rental income exceeds the limit. You only need to include your own share of the income when deciding if the rules apply.

What software can pensioners use for Making Tax Digital?

You can use HMRC-approved accounting software or spreadsheets linked to bridging software. Many pensioners may prefer simple bookkeeping software or an accountant who can handle the process for them.

If I am exempt, do I still need to report my income to HMRC?

Yes, an exemption only means you do not have to use the digital system. You must still report your income and complete a Self Assessment tax return if required.